The Great Narrowing: Venture Capital’s New Liquidity Conundrum

There was a time—not long ago, though it now feels separated from us by several geological eras of monetary policy—when venture capital resembled a broad and bustling republic. Capital flowed widely. Companies proliferated. Unicorns emerged frequently, yes, but so too did hundreds upon hundreds of smaller victories: acquisitions, IPOs, secondaries, strategic combinations.

The ecosystem breathed through volume.

That is no longer the case.

According to recent PitchBook data, the modern venture market has become astonishingly concentrated—not merely in outcomes, but in the very possibility of liquidity itself. The exit window has not disappeared. It has simply moved upward, narrowing into a tiny aperture largely accessible only to the largest celestial bodies in the venture universe.

Consider the arithmetic. In 1Q 2026, venture-backed companies raised approximately $245 billion across 227 deals. Yet five companies alone—led by OpenAI’s staggering $122 billion financing and Anthropic’s $30.6 billion raise—accounted for nearly 78% of total capital deployed.

Pause for a moment and absorb the implications of that statistic.

Hundreds of billions of dollars are indeed moving through the system, but the overwhelming majority is flowing into an extraordinarily small number of companies. Venture capital, once distributed across a broad frontier of innovation, increasingly resembles a sovereign wealth strategy directed toward a handful of AI nation-states.

And on the exit side, the concentration becomes even more dramatic. SpaceX’s $250 billion all-stock acquisition of xAI represented roughly 72.8% of the quarter’s entire $343.1 billion venture exit value. One deal. Nearly three-quarters of all liquidity.

This is not a healthy exit market. It is a statistical anomaly.

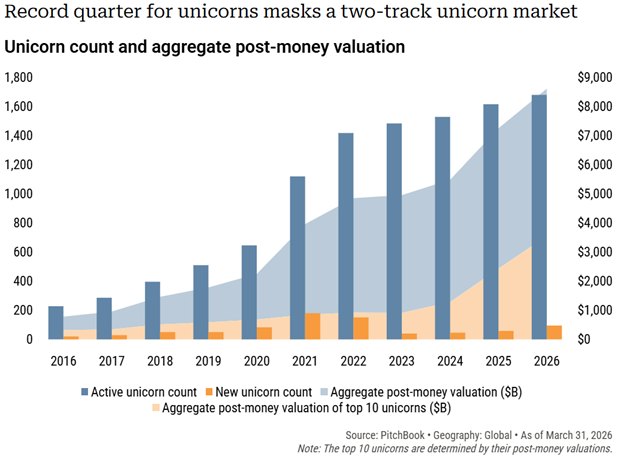

The implications are profound. Unicorns now account for approximately 74% of venture value while representing only 2.68% of deal count. In practical terms, the venture ecosystem increasingly depends upon a microscopic population of mega-companies to justify valuations, sustain LP confidence, and maintain the appearance of market vitality.

Meanwhile, beneath this glittering upper atmosphere sits the rest of the market: thousands of companies, many fundamentally sound, trapped in a liquidity drought.

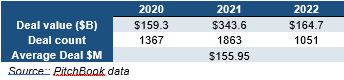

To understand the scale of the shift, compare today’s environment with the 2020–2022 period. During those years, venture activity was characterized not merely by large valuations, but by extraordinary breadth. The average deal size was approximately $156 million, and the market produced an average of 1,427 deals annually. Liquidity was democratized. Capital formation extended across stages, sectors, and geographies.

Today, volume has collapsed while capital concentration has intensified.

This creates a dangerous illusion. Headline numbers remain enormous, allowing commentators to declare that venture capital is “healthy” or “resilient.” Yet the lived reality for most founders, growth-stage companies, and general partners is radically different. Buyers remain selective. IPO windows remain largely shut outside the most elite names. Capital is available—but increasingly only for companies already perceived as inevitable winners.

Perhaps the most profound observation in the report is not the concentration of capital at the top, but the fragility of the valuations beneath it. PitchBook notes that the vast majority of unicorns—particularly those minted during the 2021 boom—have not had their valuations validated by subsequent financing rounds. Of the 473 surviving unicorns from the 2021 cohort, more than three-quarters still carry valuations established before 2023, meaning they have never been tested against post-correction market conditions. More broadly, 844 unicorns—over half the universe—have not raised capital in more than two years. In many cases, today’s “valuation” is simply the last price someone paid during a very different era of liquidity, preserved in spreadsheets like financial amber. As PitchBook bluntly observes, aggregate unicorn value is not market capitalization but “the last price someone paid for a share of each company, carried forward indefinitely until someone pays a new price.” The implication is profound: much of the venture market is not necessarily overvalued or undervalued—it is simply unpriced.

The market has become less an engine of broad innovation and more a gravitational system dominated by a few massive stars.

And therein lies the central question facing venture capital over the next several years:

Can an ecosystem built historically on breadth survive when liquidity exists almost exclusively at the summit?

Or are we witnessing the emergence of a permanently bifurcated market—one where a tiny number of AI titans absorb nearly all capital, exits, and attention while the remainder of venture capital drifts into a prolonged state of stagnant illiquidity?