The Great Narrowing: Venture Capital’s New Liquidity Conundrum

There was a time—not long ago, though it now feels separated from us by several geological eras of monetary policy—when venture capital resembled a broad and bustling republic. Capital flowed widely. Companies proliferated. Unicorns emerged frequently, yes, but so too did hundreds upon hundreds of smaller victories: acquisitions, IPOs, secondaries, strategic combinations.

The ecosystem breathed through volume.

That is no longer the case.

According to recent PitchBook data, the modern venture market has become astonishingly concentrated—not merely in outcomes, but in the very possibility of liquidity itself. The exit window has not disappeared. It has simply moved upward, narrowing into a tiny aperture largely accessible only to the largest celestial bodies in the venture universe.

Consider the arithmetic. In 1Q 2026, venture-backed companies raised approximately $245 billion across 227 deals. Yet five companies alone—led by OpenAI’s staggering $122 billion financing and Anthropic’s $30.6 billion raise—accounted for nearly 78% of total capital deployed.

Pause for a moment and absorb the implications of that statistic.

Hundreds of billions of dollars are indeed moving through the system, but the overwhelming majority is flowing into an extraordinarily small number of companies. Venture capital, once distributed across a broad frontier of innovation, increasingly resembles a sovereign wealth strategy directed toward a handful of AI nation-states.

And on the exit side, the concentration becomes even more dramatic. SpaceX’s $250 billion all-stock acquisition of xAI represented roughly 72.8% of the quarter’s entire $343.1 billion venture exit value. One deal. Nearly three-quarters of all liquidity.

This is not a healthy exit market. It is a statistical anomaly.

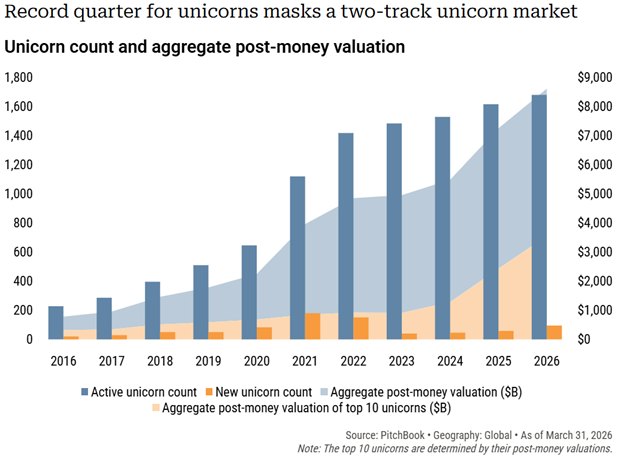

The implications are profound. Unicorns now account for approximately 74% of venture value while representing only 2.68% of deal count. In practical terms, the venture ecosystem increasingly depends upon a microscopic population of mega-companies to justify valuations, sustain LP confidence, and maintain the appearance of market vitality.

Meanwhile, beneath this glittering upper atmosphere sits the rest of the market: thousands of companies, many fundamentally sound, trapped in a liquidity drought.

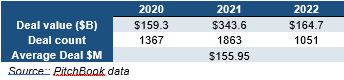

To understand the scale of the shift, compare today’s environment with the 2020–2022 period. During those years, venture activity was characterized not merely by large valuations, but by extraordinary breadth. The average deal size was approximately $156 million, and the market produced an average of 1,427 deals annually. Liquidity was democratized. Capital formation extended across stages, sectors, and geographies.

Today, volume has collapsed while capital concentration has intensified.

This creates a dangerous illusion. Headline numbers remain enormous, allowing commentators to declare that venture capital is “healthy” or “resilient.” Yet the lived reality for most founders, growth-stage companies, and general partners is radically different. Buyers remain selective. IPO windows remain largely shut outside the most elite names. Capital is available—but increasingly only for companies already perceived as inevitable winners.

Perhaps the most profound observation in the report is not the concentration of capital at the top, but the fragility of the valuations beneath it. PitchBook notes that the vast majority of unicorns—particularly those minted during the 2021 boom—have not had their valuations validated by subsequent financing rounds. Of the 473 surviving unicorns from the 2021 cohort, more than three-quarters still carry valuations established before 2023, meaning they have never been tested against post-correction market conditions. More broadly, 844 unicorns—over half the universe—have not raised capital in more than two years. In many cases, today’s “valuation” is simply the last price someone paid during a very different era of liquidity, preserved in spreadsheets like financial amber. As PitchBook bluntly observes, aggregate unicorn value is not market capitalization but “the last price someone paid for a share of each company, carried forward indefinitely until someone pays a new price.” The implication is profound: much of the venture market is not necessarily overvalued or undervalued—it is simply unpriced.

The market has become less an engine of broad innovation and more a gravitational system dominated by a few massive stars.

And therein lies the central question facing venture capital over the next several years:

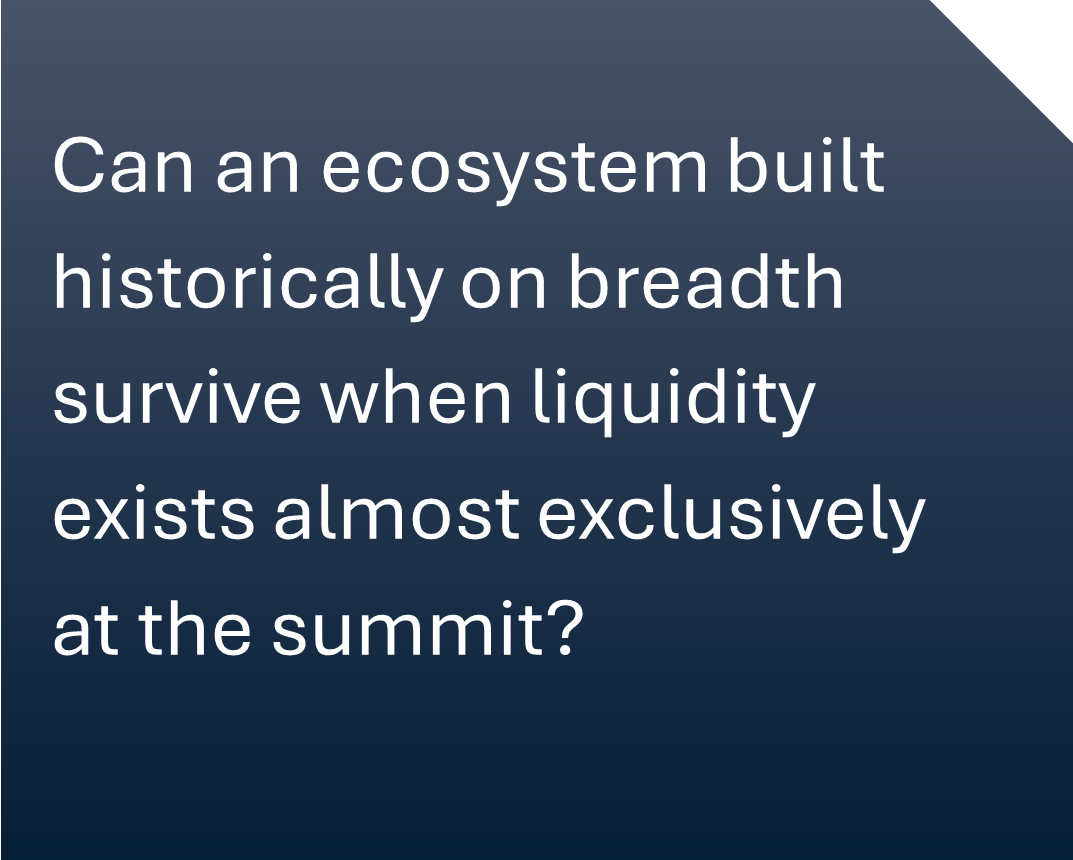

Can an ecosystem built historically on breadth survive when liquidity exists almost exclusively at the summit?

Or are we witnessing the emergence of a permanently bifurcated market—one where a tiny number of AI titans absorb nearly all capital, exits, and attention while the remainder of venture capital drifts into a prolonged state of stagnant illiquidity?

Lloyd, Where Did All the Exits Go?

A blog post from Vertical Capital Advisors with credit, where and only to the extent that arbiters and the highest court of competent jurisdiction deem us liable of expropriating theories from Stanley Bing and his seminal corporate finance masterpiece, Lloyd-What Happened: A Novel of Business.

A Memo

To: Lloyd

From: The Architect

Date: 9/16/2025

Lloyd, my friend.

Do you remember when the world was simple?

You invested in a company—call it SaaS, call it AI, call it “next-gen quantum-enabled dog food”—and two or three years later, someone rang the bell. IPO! Confetti, roadshows, a ticker symbol so shiny it made angels sing. Or, barring that, a strategic acquirer with more dollars than sense showed up, signed a term sheet, and whisked your portfolio company away to the land of liquidity.

That was then.

Now? We sit on a billion dollars of promise. A billion! A serious fund. A weighty fund. A fund with gravitas. A fund whose quarterly reports feature graphics so elegant they make LPs weep with joy. And yet, despite this abundance of presentation, something troubling lurks: The exits, Lloyd. They are gone. We once had a rhythm. Capital goes in, multiples come out. IPOs like buses—miss one, wait five minutes, there’s another. Now, buyers are “evaluating.” Translation: they are in conference rooms stroking their chins, producing PowerPoint decks with titles like “Strategic Capital Deployment Options in a Disciplined Environment.” Which is corporate dialect for “We’re not buying anything, ever.”

Instead of champagne corks popping, we find ourselves staring at the liquidity window like monks waiting for enlightenment. The IPO market, they tell me, is “cooling.” Translation: shut tight, drafty at the edges, and guarded by men with clipboards.

Strategic buyers? They circle, they sniff, they nod sagely, and then they retreat to their “capital allocation committees.” Which, if you haven’t noticed, are really just padded rooms with whiteboards where ideas go to die.

Meanwhile, the companies - our companies - keep raising, but only from insiders. We shovel good money after the already-invested money, because who else will? Outsiders are shy. “Valuations are high,” they mutter. Of course they’re high! That was the point, Lloyd.

And have you noticed the math? For every six expansion-stage investments, there’s but one lonely exit. A ratio not of abundance, but of constipation. The pipeline bulges, but the valve will not open.

Our LPs call. They ask, ever so sweetly: “When might we expect DISTRIBUTIONS?” We assure them, with the confidence of medieval astrologers, that Jupiter is in retrograde and SaaS multiples will rise again. In the meantime, please admire this waterfall chart, color-coded for your convenience.

We were told geography might help. Baltimore, they whispered. Energy deals in Houston. Health tech in DC. But exits are still hoarded by the same gilded hubs—New York, San Francisco—like dragon treasure, inaccessible to the brave yet undercapitalized knights of secondary markets.

And so we wait. Our LPs ask when distributions will come, and we smile the smile of those who do not know. We point to AI, to manufacturing, to SaaS. We say, “There is momentum.” But inside, we feel the wobble. Momentum is wonderful until you realize you’re running downhill and the brakes don’t work.

What does one do, Lloyd, when one cannot exit? One writes whimsical memos. One becomes mystical. One contemplates liquidity not as an event but as a state of being. Perhaps liquidity is enlightenment. Perhaps exits are illusions. Perhaps the true return is the friends we made along the way.

Sidebar, Lloyd. Have you noticed how the vocabulary itself betrays us?

Once, we spoke of ROI—a quaint, earthy metric. Money in, more money out. A ratio you could explain to your aunt at Thanksgiving. Ah, return on investment, wherefor art thou?

Then, in our sophistication, we ascended to MOIC. Multiple on Invested Capital. It sounded grand, didn’t it? A multiple! A multiplication! As though we were magicians. But MOIC is a mirage, Lloyd. It glows on paper, yet remains stubbornly unconverted.

And finally, the cruelest of them all: DPI. Distributions to Paid-In. Not theoretical, not pro forma, but actual, cold cash returned. And it is here, Lloyd, where the dream falters. For there are no exits, and thus no distributions.

Perhaps this progression is the curse itself: ROI begat MOIC begat DPI, and somewhere along the way the gods of liquidity grew tired of our acronyms. (See Exhibit D: Tower of Metric Babel.)

Is it the markets that have failed us, Lloyd—or simply the metrics we chose to worship?

Lloyd, perhaps the problem is not exits at all, but measurement. ROI, MOIC, DPI—these were mile markers on a road that has vanished into mist. So what comes next?

I propose HFI: Hopefulness per Fund Interval.

It measures not cash returned, nor multiples achieved, but the sheer buoyancy of spirit with which a GP explains, quarter after quarter, why liquidity is “just around the corner.”

Others may prefer LOL: Longevity of LP Patience, or perhaps the darker SIGH: Self-Inflicted GP Hand-wringing.

But HFI, Lloyd—that feels right. It captures the essence of our age: no exits, no distributions, just optimism compounded annually.

And so we enter a new spiritual phase of fund management. We meditate on liquidity. We redefine “exit” as not an event, but a state of mind. We speak of “patient capital” while somewhere, an acquirer is squinting at a data room. Somewhere, an IPO window is cracking open. Somewhere, perhaps, the great Wheel of Liquidity will turn again and Vanna will turn our magic letter.

Let us float above our billion-dollar dilemma as though we are not trapped in it, but merely observing from a higher plane. After all, it is only money.

And yet…

Lloyd. Truly.

Where did all the exits go?

Private Markets Pulse: Investments vs Exits in Q3 2025

We’re seeing a shift in the private financial markets this quarter—one that feels less like steady growth, more like recalibration. Expansion-stage exits are coming back into focus, investor strategies are evolving, and liquidity is increasingly a central concern. As macroeconomic uncertainty lingers, participants are adjusting expectations, pacing, and risk tolerance.

The Lay of the Land

We’re seeing a shift in the private financial markets this quarter—one that feels less like steady growth, more like recalibration. Expansion-stage exits are coming back into focus, investor strategies are evolving, and liquidity is increasingly a central concern. As macroeconomic uncertainty lingers, participants are adjusting expectations, pacing, and risk tolerance.

Key Themes

Here are the trends that stood out most to me from Deloitte’s latest report:

Exit Value Rebounding, But With Caveats

Expansion-stage exit value is on the upswing in 2025. Manufacturing and AI (including AI-adjacent SaaS businesses) are leading the way. Still, IPOs—even though some marquee successes are shining—have cooled relative to their peaks. The message: there’s interest, but volatility and public-market conditions are tempering enthusiasm. (Deloitte)Investor Behavior Shifting

Dry powder for VCs dropped in 2024, which tells us more capital is being deployed. (Deloitte)

Portfolio valuations remain elevated. That means LPs are increasingly focused on when and how liquidity events will happen. The old maxim “cash is king” feels newly relevant.

Insider rounds (follow-on funding from existing investors) are surging. For expansion stage firms, that signals a preference for backing what’s known vs introducing new risk. (Deloitte)

Liquidity & Exit Pace Lagging Investment Pace

Perhaps the biggest tension point: investments, especially in the expansion stage, are growing faster than exits. Deloitte notes a ratio of 5.7x for expansion-stage investments to exits in the first half of 2025. That discrepancy raises questions about how long dry or illiquid this environment may be for many portfolios. (Deloitte)Geographic & Sector Nuance

Traditional hubs (think New York, Bay Area) still dominate when it comes to exit activity. That’s not a surprise. But secondary cities are tightening their grip in certain verticals—particularly health care and energy. Washington, DC and Baltimore are named as examples. (Deloitte)

Sectors with strong tailwinds: high-value manufacturing, AI, SaaS. These are attracting serious exit interest. However, manufacturing exits seem boosted by a few outlier deals, so we should watch for how representative those are in the aggregate. (Deloitte)

Implications for Investors & Founders

What do these trends mean, in practice?

Founders: If you’re leading an expansion-stage company, your exit strategies may need to be more creative. Traditional IPOs are still possible, but many will look to trade sales, strategic acquirers, or structuring follow-on rounds with insider support.

Investors / LPs: Guard against complacency around valuation inflation. Because valuations remain high, exit multiples may compress when exits do happen (if market sentiment doesn’t fully sync). Maintaining flexibility and choosing contracts that allow for optionality (such as exit rights, secondary markets, etc.) may be wise.

Deal Flow Timing and Pacing: Given the lag in exits vs investments, there may be a build-up of pressure for liquidity. This could push some exits to market sooner than expected, or force restructuring of expectations for what returns will look like.

Geographic Opportunity: Secondary markets—in energy and healthcare particularly—look like fertile ground. If you’re evaluating deal opportunities outside of the core hubs, there’s rising evidence that those may offer differentiated return potential (and perhaps less froth in valuations).

What to Watch Next

To stay sharp, I’m keeping eyes on:

Whether the investment-to-exit ratio begins to close. If that gap remains wide, it could signal bottlenecks in the exit pipeline or down-round risk.

Public market volatility—especially around macroeconomic data, interest rates, inflation, and regulatory developments. Those will continue to influence IPO window strength.

How sectors outside AI/SaaS/manufacturing fare. Are newer sectors starting to break through, or will strength concentrate further in what’s already hot?

The movement of capital into secondary and tertiary cities. Whether infrastructure, regulation, or incentives will make those markets more competitive overall.

Bottom Line

Right now, private markets feel like they’re in a holding pattern of sorts—passionate about forward momentum, but waiting for clear skies before making bold moves. For founders, investors, and dealmakers, the key will be balancing optimism with realism: striving for exit opportunities but preparing for scenarios where liquidity comes on others’ terms.

Is Your Business Ready for a Capital Raise? 5 Signs to Look For

Raising outside capital is a big step for any company. It can unlock new growth opportunities, whether you're looking to expand operations, invest in new technology, or acquire another business. However, wanting to raise capital and being ready to do so are two very different things.

Raising outside capital is a big step for any company. It can unlock new growth opportunities, whether you're looking to expand operations, invest in new technology, or acquire another business. However, wanting to raise capital and being ready to do so are two very different things.

Savvy investors, lenders, and partners look for specific indicators of readiness before they commit funds. Understanding these signs can give your business a significant edge.

Here are five key signs that your business might be ready for a capital raise.

1. You Have a Scalable Growth Plan

A compelling vision is great, but investors need to see a concrete plan for how their money will lead to profitable growth. This means you've done the groundwork and can clearly demonstrate:

A well-defined market opportunity.

Product-market fit that's been validated.

Realistic growth milestones and a clear understanding of the funding needed to hit them.

If your growth is currently limited by things like a lack of working capital or infrastructure, and you can show how an investment would directly solve that problem, you're sending a strong signal that you're ready.

2. Your Financials Are Flawless

Any potential investor will thoroughly scrutinize your financials. They expect to see clean, consistent, and transparent records. Key expectations include:

GAAP-compliant (or near-compliant) reporting.

Consistent revenue recognition practices.

Well-organized books, preferably reviewed by an external accountant.

Reasonable forecasts that are supported by historical data.

If your financial house isn't completely in order yet, that's okay. Many businesses need help preparing their financial story for the scrutiny of the capital markets.

3. You Understand Your Capital Needs and Options

Are you seeking equity, debt, convertible notes, or a combination? Do you know exactly how much you need and how long it will last?

Sophisticated founders know that the structure of the capital is just as important as the amount. The clearer you are about the type of capital you're looking for and your reasons for seeking it, the easier it will be to attract the right partner.

4. You Have the Right Team in Place

Capital follows confidence, and nothing inspires confidence like a strong leadership team. Investors aren't just betting on your idea; they're betting on your ability to execute it.

Signs you're ready to raise capital:

You have a CEO who can articulate the company's story with clarity and conviction.

A CFO or controller is on board who can handle due diligence questions.

Your functional leaders (in sales, operations, and technology) have a proven track record.

If you've been running the show solo, it might be time to build out your team before you approach investors.

5. You've Already Invested in the Business

Investors want to see that you have "skin in the game." This could mean a personal financial investment, reinvested profits, or significant sweat equity. What's important is that you've already committed meaningful resources to get the business to its current point.

This commitment signals that you truly believe in the opportunity and that you're looking for a partnership, not an exit strategy.

Final Thoughts

Raising capital is more than just getting a check; it's about building a business that's inherently investable. The earlier you start preparing for this process, the smoother your capital raise will be when the time comes.

If you're wondering whether your business is ready for a capital raise, our team can help you assess your current position and build a smart path forward.

Do you want to know where your business stands? Schedule a 30-minute Capital Readiness Assessment with our advisory team today.

It’s not you, it’s m…(the market)

The Roaring 20’s. Well, it was really just 2021 but what a year it was! At the lower end of the middle market where Vertical Capital Advisors does most of our work, 4Q2021 saw a record $190B in early stage investing globally which dropped precipitously to $62.2B by 4Q2023, rebounding only slightly to $66.1B in the first quarter of 2024 according to Crunchbase:

Source: https://news.crunchbase.com/venture/startup-funding-q1-2024-charts/

Anyone seeking venture, start-up or growth capital and even traditional M&A and strategic partnerships felt the pinch last year. Capital allocators including banks pumped the brakes as inflation and interest rates surged while everyone sat in their perches scouring the horizon for the next macroeconomic event to crest. Most are still waiting.

So, it’s not you, it’s the market. If you have been doing all of the actions that smart, adaptable business owners do but found little interest from capital sources in funding your growth, you are not alone. Most businesses experienced a slowdown in funding and deals that normally would have been funded find themselves waiting patiently for the markets to normalize.

What can you do if your business needs capital now? If you have exhausted all of your efforts to find a capital partner, find a professional with a large network who can help you cast a broader net and be prepared to extend your timeline. It will take longer to get your deal funded. Also explore the use of technology to enhance your outreach. We are doing that now using AI tools to extend our reach and engage with far more individuals than we can realistically contact directly. Great opportunities will get funded, it will just take more creativity and time to get there.

* * *

ABOUT VERTICAL CAPITAL ADVISORS

Vertical Capital Advisors is an Atlanta-area boutique investment banking firm built on creating tangible value for our clients, serving clients in just about every industry. Our clients are both capital growers and capital allocators. How can Vertical help your firm maximize value?

Carolyn Briner

Managing Director

Vertical Capital Advisors LLC

cbriner@verticalcapitaladvisors.com

866-912-9543 ext 108

678-591-4804