VC Funding: Overhang, or Cliff?

Crunchbase News reported on Wednesday that VC funding hasn’t seen a massive downturn… yet.

The basic thesis is a good one and backed up by experienced history: VC funding normally gets hit when market crashes occur. It happened in 2001, and again in 2008-2009.

Clearly, equity markets are crashing, reflecting investors views on future (albeit relatively near-term future) corporate earnings. When VC/PE funding slows, there is an inevitable knock-on effect: IPO’s slow or stop, and investors pull back from funding loss-making startups.

So where are we right now (i.e., this week)? Well, we aren’t yet at the funding famine stage but we could be well down the road. It’s hard to say, but we’ll certainly know in another month or so.

If we compare Q1 2019 to Q1 2020 (according to Crunchbase) we see that total VC deals for the two periods are pretty close but that 2020 is still about 12.4% lower:

Q1 2019 VC Funding Deals:

Difference between VC funding deals in Q1 2019 and Q1 2020, deals over $10 million. (Source: Crunchbase)

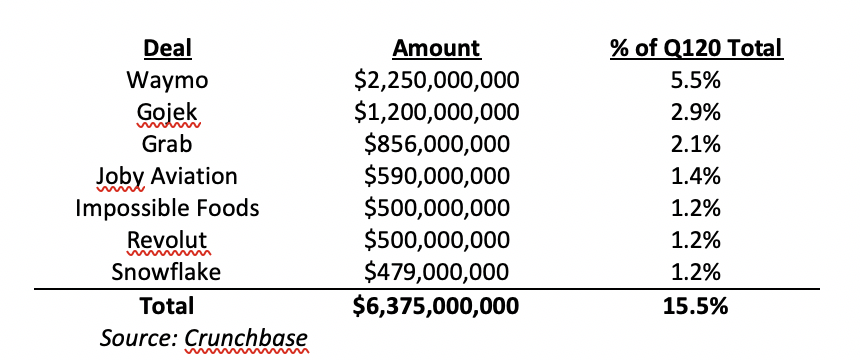

However, keep in mind that “Monster” Deals comprised about 15.5% of the total for Q1 2020 (see the table below). If you take these deals out of the mix, the difference between the two time periods grows considerably, from 12.4% to 33%. That’s a more significant and eye-catching number, and since it almost certainly can’t be attributed to either current market conditions or COVID-19, it’s also worth exploring in more detail in a later post.

Also, there is usually quite a bit of lag time between when funding is agreed and the round is actually closed. So many of the deals that are closing in Q1 2020 were almost certainly agreed in late 2019. There’s a time lag at work here.

As a result, we almost certainly haven’t yet seen VC funding deals fall off the cliff… but it’s probably coming, and we won’t see it in the data for another couple of months.

There is a potential bright spot that was foreshadowed earlier in this article: that is, VC funding for loss-making startups and businesses (bankrolling losses in the hope of future growth) will almost certainly dry up.

But if you are profitable – or very close to it – you may be in a better position than you were just a couple of months ago.

In any case, it’s likely that future data will show the VC and PE funding overhang to have fallen off a cliff – but it probably won’t dry up completely for profitable or near-profitable businesses.

James Cooper

Principal, Vertical Capital Advisors

jcooper@verticalcapitaladvisors.com