VC Funding: Overhang, or Cliff?

VC funding hasn’t seen a massive downturn… yet. But have we already gone over the cliff? The data is backward looking, so the cliff may be close than it appears.

Crunchbase News reported on Wednesday that VC funding hasn’t seen a massive downturn… yet.

The basic thesis is a good one and backed up by experienced history: VC funding normally gets hit when market crashes occur. It happened in 2001, and again in 2008-2009.

Clearly, equity markets are crashing, reflecting investors views on future (albeit relatively near-term future) corporate earnings. When VC/PE funding slows, there is an inevitable knock-on effect: IPO’s slow or stop, and investors pull back from funding loss-making startups.

So where are we right now (i.e., this week)? Well, we aren’t yet at the funding famine stage but we could be well down the road. It’s hard to say, but we’ll certainly know in another month or so.

If we compare Q1 2019 to Q1 2020 (according to Crunchbase) we see that total VC deals for the two periods are pretty close but that 2020 is still about 12.4% lower:

Q1 2019 VC Funding Deals:

Difference between VC funding deals in Q1 2019 and Q1 2020, deals over $10 million. (Source: Crunchbase)

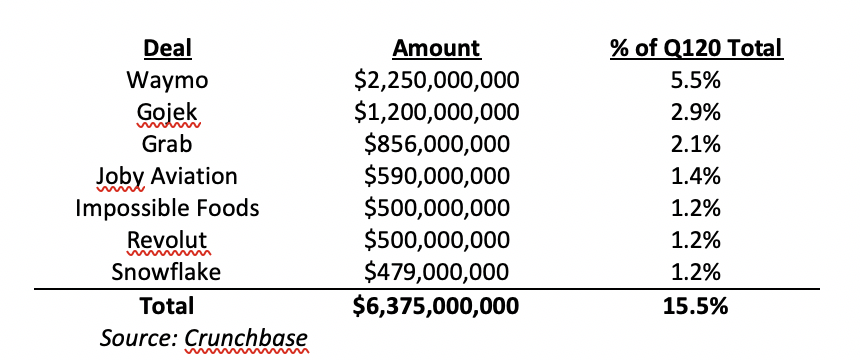

However, keep in mind that “Monster” Deals comprised about 15.5% of the total for Q1 2020 (see the table below). If you take these deals out of the mix, the difference between the two time periods grows considerably, from 12.4% to 33%. That’s a more significant and eye-catching number, and since it almost certainly can’t be attributed to either current market conditions or COVID-19, it’s also worth exploring in more detail in a later post.

Also, there is usually quite a bit of lag time between when funding is agreed and the round is actually closed. So many of the deals that are closing in Q1 2020 were almost certainly agreed in late 2019. There’s a time lag at work here.

As a result, we almost certainly haven’t yet seen VC funding deals fall off the cliff… but it’s probably coming, and we won’t see it in the data for another couple of months.

There is a potential bright spot that was foreshadowed earlier in this article: that is, VC funding for loss-making startups and businesses (bankrolling losses in the hope of future growth) will almost certainly dry up.

But if you are profitable – or very close to it – you may be in a better position than you were just a couple of months ago.

In any case, it’s likely that future data will show the VC and PE funding overhang to have fallen off a cliff – but it probably won’t dry up completely for profitable or near-profitable businesses.

James Cooper

Principal, Vertical Capital Advisors

jcooper@verticalcapitaladvisors.com

Private Equity 2020

Something funny is going in Private Equity in 2020… the right guide will get you safely over the whitewater so you can enjoy the view from the other side.

Private Equity in 2020 in Three Charts

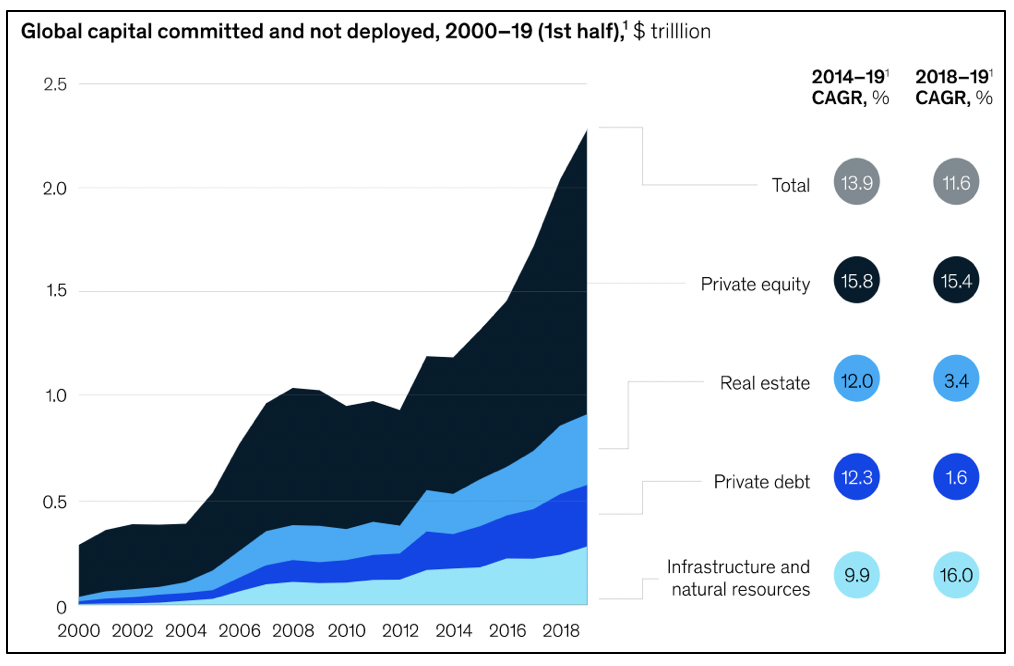

When capital markets are more flush than ever with cash …

Source: McKinsey & Co.

Source: Bain & Co.

prices are driven up…

resulting in exit multiples remaining stable despite improving revenue, margins and multiples!

Wait. That makes no sense!

More money than ever pushing prices up yet exit multiples remain flat – what’s going on?

Source: Bain & Co.

No revenue growth, no margin expansion, no multiple expansion

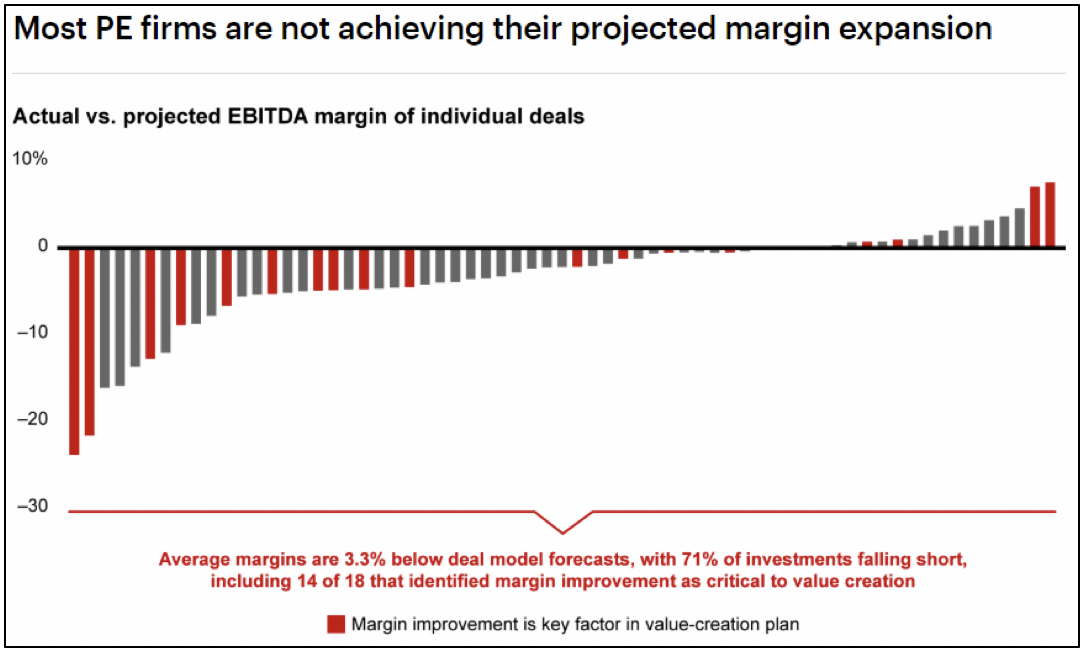

Most private equity firms are reducing their estimates of multiple expansion given the worsening macroeconomic trends and decade-long secular trend of increasing deal multiples, and as revenue growth slows or reverses in a soft economy, the two primary drivers of incremental deal value are compromised. And because 71% of deals fail to deliver margin expansion even when margin expansion is a key driver of expected performance (see Bonus Chart 1 below), all three legs of the growth engine are compromised.

Bonus Chart 1 (Source: Bain & Co.)

What this means for you

What does this mean for US and international small to medium sized businesses? First, with all of the committed cash on the sidelines, investors are going to be hungry for deals – they will be spending. Many institutional investors may choose to delay investment decisions or make more opportunistic investments and acquisitions as economic conditions deteriorate (BTW, opportunistic is often a euphemism for distressed – as a business owner you do not want to be in this category – ever). You can expect longer due diligence periods and attempts to renegotiate deal terms as your deal moves from indication of interest (IOI) to letter of interest (LOI) to term sheet to subscription agreement or purchase and sale agreement. Having an experienced guide to insulate you from as much of the back and forth as possible, allowing you to focus on continued peak performance of your business is critical. We saw these things occur during the 2008-2010 Great Recession and other periods of economic turmoil. Turmoil and the uncertainty it breeds are not your friend. The right guide will get you safely over the whitewater so you can enjoy the view from the other side.

Congratulations on reading this far - here’s a second bonus chart to reward you for your effort. If you have sensed that private equity has grown to be a more significant part of the global financial picture than public equities (stocks that are publicly traded on exchanges like the New York Stock Exchange or NASDAQ), you are right:

Bonus Chart 2 (Source: McKinsey & Co.)

Private equity is now nearly four times larger than public equity yet world financial markets revolve around public equities. Ironically, initial public offerings (IPOs) are still a favorite exit strategy for large private equity firms. So don’t panic when you see markets gyrating. The median holding period for private equity investments is 4.3 years (Source: Bain). A well-run business will navigate the turmoil and probably emerge stronger having had to make tough decisions about every aspect of the business.

Vertical Capital Advisors can help your business plan and execute strategies that enable your enterprise to thrive in all market conditions. It’s not too late to plan. Call us today.

* * *

ABOUT VERTICAL

Vertical Capital Advisors is an Atlanta-area boutique investment banking firm built on creating tangible value for our clients, serving clients in just about every industry. Our clients are both capital growers and capital allocators. How can Vertical help your firm maximize value?

Joe Briner

Managing Director

Vertical Capital Advisors LLC

briner@verticalcapitaladvisors.com

866-912-9543 ext 108

678-591-0273