VC Funding: Overhang, or Cliff?

VC funding hasn’t seen a massive downturn… yet. But have we already gone over the cliff? The data is backward looking, so the cliff may be close than it appears.

Crunchbase News reported on Wednesday that VC funding hasn’t seen a massive downturn… yet.

The basic thesis is a good one and backed up by experienced history: VC funding normally gets hit when market crashes occur. It happened in 2001, and again in 2008-2009.

Clearly, equity markets are crashing, reflecting investors views on future (albeit relatively near-term future) corporate earnings. When VC/PE funding slows, there is an inevitable knock-on effect: IPO’s slow or stop, and investors pull back from funding loss-making startups.

So where are we right now (i.e., this week)? Well, we aren’t yet at the funding famine stage but we could be well down the road. It’s hard to say, but we’ll certainly know in another month or so.

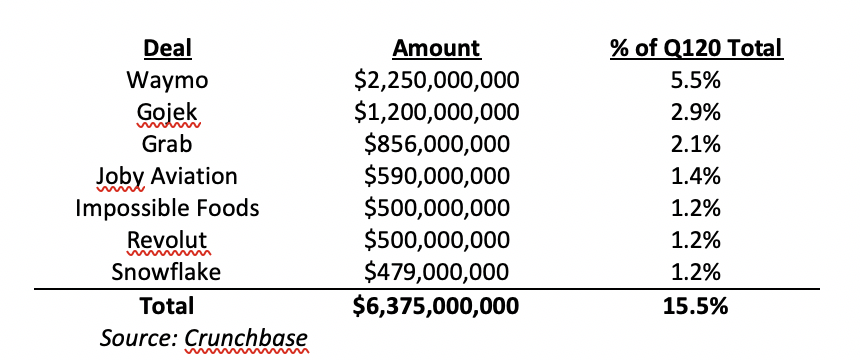

If we compare Q1 2019 to Q1 2020 (according to Crunchbase) we see that total VC deals for the two periods are pretty close but that 2020 is still about 12.4% lower:

Q1 2019 VC Funding Deals:

Difference between VC funding deals in Q1 2019 and Q1 2020, deals over $10 million. (Source: Crunchbase)

However, keep in mind that “Monster” Deals comprised about 15.5% of the total for Q1 2020 (see the table below). If you take these deals out of the mix, the difference between the two time periods grows considerably, from 12.4% to 33%. That’s a more significant and eye-catching number, and since it almost certainly can’t be attributed to either current market conditions or COVID-19, it’s also worth exploring in more detail in a later post.

Also, there is usually quite a bit of lag time between when funding is agreed and the round is actually closed. So many of the deals that are closing in Q1 2020 were almost certainly agreed in late 2019. There’s a time lag at work here.

As a result, we almost certainly haven’t yet seen VC funding deals fall off the cliff… but it’s probably coming, and we won’t see it in the data for another couple of months.

There is a potential bright spot that was foreshadowed earlier in this article: that is, VC funding for loss-making startups and businesses (bankrolling losses in the hope of future growth) will almost certainly dry up.

But if you are profitable – or very close to it – you may be in a better position than you were just a couple of months ago.

In any case, it’s likely that future data will show the VC and PE funding overhang to have fallen off a cliff – but it probably won’t dry up completely for profitable or near-profitable businesses.

James Cooper

Principal, Vertical Capital Advisors

jcooper@verticalcapitaladvisors.com

Private Equity 2020

Something funny is going in Private Equity in 2020… the right guide will get you safely over the whitewater so you can enjoy the view from the other side.

Private Equity in 2020 in Three Charts

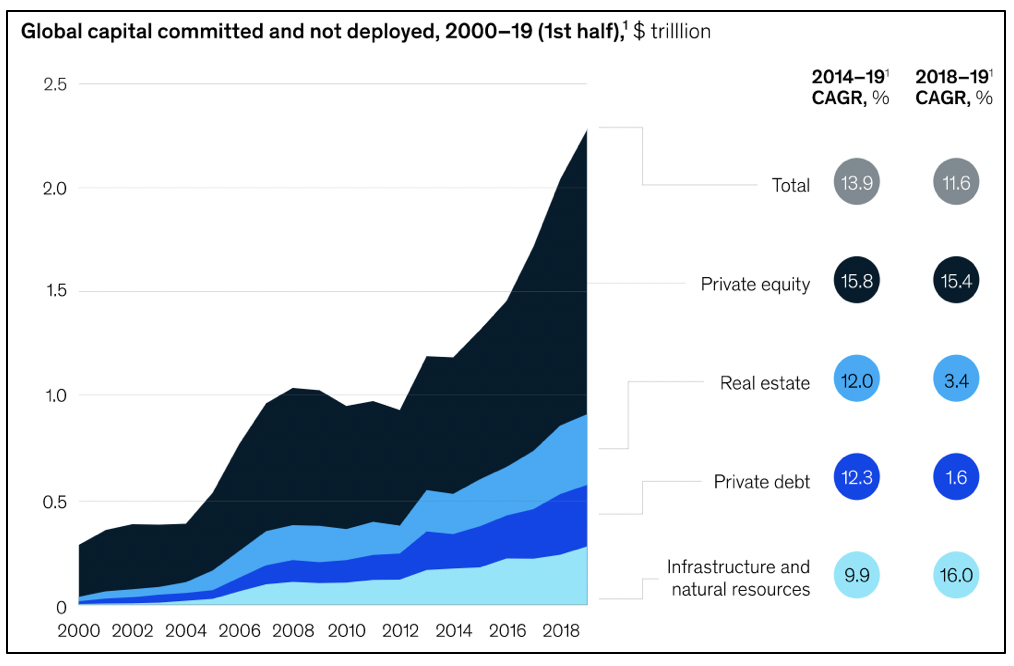

When capital markets are more flush than ever with cash …

Source: McKinsey & Co.

Source: Bain & Co.

prices are driven up…

resulting in exit multiples remaining stable despite improving revenue, margins and multiples!

Wait. That makes no sense!

More money than ever pushing prices up yet exit multiples remain flat – what’s going on?

Source: Bain & Co.

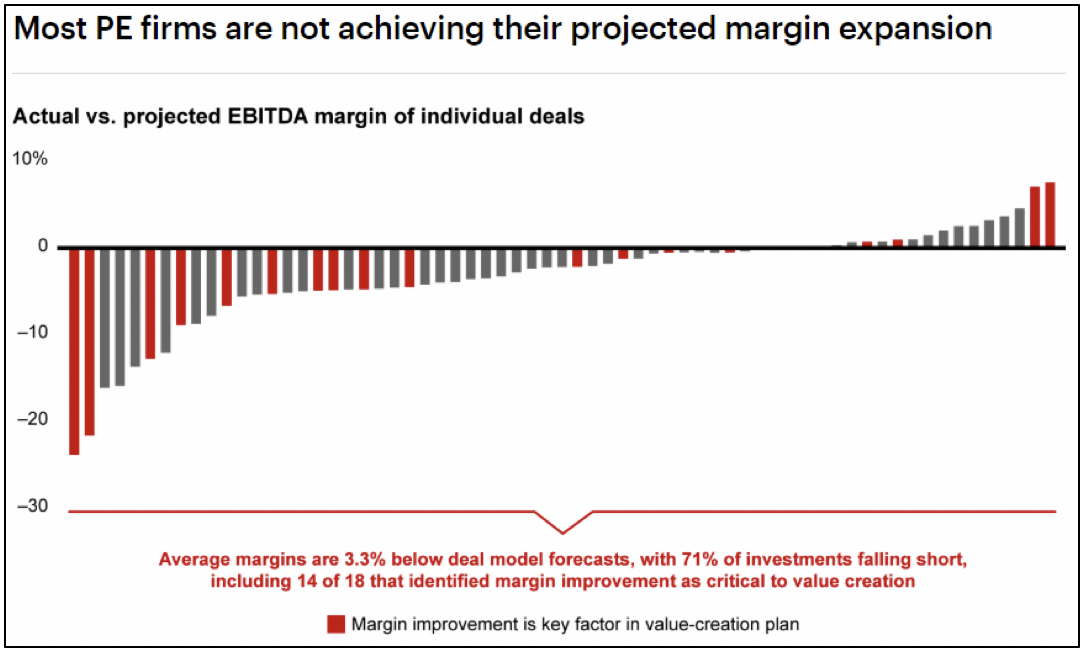

No revenue growth, no margin expansion, no multiple expansion

Most private equity firms are reducing their estimates of multiple expansion given the worsening macroeconomic trends and decade-long secular trend of increasing deal multiples, and as revenue growth slows or reverses in a soft economy, the two primary drivers of incremental deal value are compromised. And because 71% of deals fail to deliver margin expansion even when margin expansion is a key driver of expected performance (see Bonus Chart 1 below), all three legs of the growth engine are compromised.

Bonus Chart 1 (Source: Bain & Co.)

What this means for you

What does this mean for US and international small to medium sized businesses? First, with all of the committed cash on the sidelines, investors are going to be hungry for deals – they will be spending. Many institutional investors may choose to delay investment decisions or make more opportunistic investments and acquisitions as economic conditions deteriorate (BTW, opportunistic is often a euphemism for distressed – as a business owner you do not want to be in this category – ever). You can expect longer due diligence periods and attempts to renegotiate deal terms as your deal moves from indication of interest (IOI) to letter of interest (LOI) to term sheet to subscription agreement or purchase and sale agreement. Having an experienced guide to insulate you from as much of the back and forth as possible, allowing you to focus on continued peak performance of your business is critical. We saw these things occur during the 2008-2010 Great Recession and other periods of economic turmoil. Turmoil and the uncertainty it breeds are not your friend. The right guide will get you safely over the whitewater so you can enjoy the view from the other side.

Congratulations on reading this far - here’s a second bonus chart to reward you for your effort. If you have sensed that private equity has grown to be a more significant part of the global financial picture than public equities (stocks that are publicly traded on exchanges like the New York Stock Exchange or NASDAQ), you are right:

Bonus Chart 2 (Source: McKinsey & Co.)

Private equity is now nearly four times larger than public equity yet world financial markets revolve around public equities. Ironically, initial public offerings (IPOs) are still a favorite exit strategy for large private equity firms. So don’t panic when you see markets gyrating. The median holding period for private equity investments is 4.3 years (Source: Bain). A well-run business will navigate the turmoil and probably emerge stronger having had to make tough decisions about every aspect of the business.

Vertical Capital Advisors can help your business plan and execute strategies that enable your enterprise to thrive in all market conditions. It’s not too late to plan. Call us today.

* * *

ABOUT VERTICAL

Vertical Capital Advisors is an Atlanta-area boutique investment banking firm built on creating tangible value for our clients, serving clients in just about every industry. Our clients are both capital growers and capital allocators. How can Vertical help your firm maximize value?

Joe Briner

Managing Director

Vertical Capital Advisors LLC

briner@verticalcapitaladvisors.com

866-912-9543 ext 108

678-591-0273

Surprise Fed Rate Cut

In light of the Fed’s recent ‘emergency’ rate cut, we have to ask: Does this action do anything to help fight the public health crisis presented by COVID-19? No. The Fed’s action does nothing to solve the underlying problem we are facing. That is, getting to grips with the virus’ spread, testing, containment, and developing an effective vaccine.

Thoughts on the Surprise Fed Rate Cut

'Oh ok, so what? It isn’t a vaccine'

In light of the Fed’s recent ‘emergency’ rate cut, we have to ask: Does this action do anything to help fight the public health crisis presented by COVID-19?

No.

The Fed’s action does nothing to solve the underlying problem we are facing. That is, getting to grips with the virus’ spread, testing, containment, and developing an effective vaccine.

Rate cuts don’t help on the ground with the real issues people are facing and are likely to face in the coming weeks.

What’s needed is quick medical and scientific progress in treating the disease. Inflamed and misleading political rhetoric, a distrust of science, and Fed panic in relation to short-term market reactions don’t help.

This appears to be the view of other experienced investors, including Dr. Mohammed El-Erian, (Chief Economic Advisor at Allianz) and Dr. Komal Sri-Kumar (CEO of Sri-Kumar Global Strategies), so I feel like I’m in good company.

(Note: Dr. El-Erian also makes the salient point that the Fed can’t have it both ways: It can’t say that the economy is strong, then turn around in the same breath and say that we are in an emergency situation. Mixed messages to be sure, and food for thought about whether the Fed knows something that nobody else knows. It also raises questions about the Fed’s independence - an issue I refuse to address right now!)

Another way of putting it is:

A rate cut will not help people if they are home sick and afraid;

A rate cut won’t help businesses that can’t open because their employees can’t come in to work;

A rate cut won’t help people that are living month-to-month pay their bills or feed their kids;

A rate cut won’t help uninsured or under-insured people get the medical care they may need;

A rate cut won’t help identify existing cases of COVID-19, prevent future cases, or treat people that get ill;

A rate cut won’t provide testing kits and facilities that work as required; and

A rate cut won’t develop a vaccine.

It might help refinance a mortgage, or allow a business to refinance long term debt. But I’m pretty certain that there is no Fed rate cut in any possible universe that can convince people that they are not at risk of getting sick. And I’m pretty sure that if they are already sick, or afraid of getting sick, their first thought isn’t going to be that they can get a pretty attractive fixed rate refi right now.

However, reasonable questions might include,

Will this move prove to have been economically wise and far-sighted, or will it be viewed as a case of the Fed being mis-guided by market volatility and twitter storms?

Was it wise to shoot irreplaceable bullets now when they might be more useful in the future when the true economic situation is known?

And in any case, what’s the harm?

Whether the emergency cut was wise or a mis-use of scarce policy resources remains to be seen. We’ll know at some point in the future. It’s clear that folks who earn their daily bread from trading the markets think it’s great.

The fact is, however, that the Fed didn’t have much dry powder last week to address serious longer term challenges. It has even less today.

As Joe Briner, Principal at Vertical Capital Advisors noted, “...they [the Fed] literally have one tool in their toolkit: the fed funds target rate. They implement policy through open market operations which affects a lot of other things, but when all you have is one hammer, every problem can only be a nail.”

Dr. El-Erian points out that there are actually three reasons that this move could cause harm: First, the Fed’s gamble has reduced the number of available options for the future no matter what the economic outcome. That can’t be good. Second, Governments need to use the right tool for the problem. Not only is the Fed the wrong agency but the fed funds rate is the wrong tool. It’s like the Braves calling a plumber to close out the 9th inning. Finally, it’s unclear what this move does to the Fed’s credibility. Clear forward guidance is an important policy tool, and it’s not certain that Chairman Powell and the Board have enhanced their credibility or not.

As for fiscal policy options, those seem limited as well. With deficits on pace to exceed $1 trillion per year over the next decade (!!) and limited tax receipts, it is unlikely that the Government can follow South Korea’s excellent lead by announcing a significant stimulus.

For clarity, the South Korean government just announced a $9.8 billion stimulus to help counter the economic impact - the funds will go to real services and meet real needs in the on-the-ground economy by focusing on health system, child care, and outdoor markets. An equivalent stimulus in the US on a per capita basis would need to exceed $51 billion.

Also - virus testing in Korea is both free and very widespread… something that is necessary to control pandemic illnesses, but isn’t likely to happen here. It may not seem like much, but the South Korean response is far more pragmatic and focused on real problems. The Fed, on the other hand, speaks in abstractions like ‘economic activity,’ ‘solid growth’ and ‘labor market.’ Contrast that to Finance Minister Hong Nam-ki who speaks about vulnerable sectors, small- and medium-sized businesses and business owners, and self employed people.

The difference may be subtle, but it’s there.

More positive is the news that Congress is working to pass a bill providing almost $8 billion in funding to fight this outbreak. It’s a good start, and it will definitely help. Even better, it’s bi-partisan (a bit of good news we all need right now).

But because I’m a bit of a curmudgeon, I am compelled to question whether the cows have already left the barn, and whether it’s better to think of this bill to be an amuse-bouche or appetizer rather than the main course.

Even the World Bank has just announced a $12 billion commitment to help countries battling the virus. Throwing money at a problem never makes it go away, but it can help if it’s used the right way.

As Bridgewater Associates’ CIO Ray Dalio says:

“...as far as central bank policies are concerned, interest-rate cuts and increased liquidity won’t lead to any material pickup in buying and activity from people who don’t want to go out and buy, though they can goose risky asset prices a bit at the cost of bringing rates closer to hitting ground zero… So, it seems to me that containing the economic damage requires coordinated monetary and fiscal policy targeted more at specific cases of debt/liquidity-constrained entities rather than more blanket cuts in rates and broad increases in liquidity.”

Two final thoughts:

Use the right tool for the job. Don’t use a hammer when a scalpel is needed. But if you insist on using a hammer, be realistic about the results you can expect.

When it comes to dealing with this emerging public health crisis, let’s agree that we should be focused on people - not markets.

James Cooper

Vertical Capital Advisors

March 4, 2020

Why the rollercoaster market?

Why is the market so volatile? What’s going on?

Why is every day like Mr. Toad’s Wild Ride? Might be the Night of the Long Knives…

Yes, it seems that Mr. Toad grabbed the controls on October 1, taking the market on a wild ride. Take a look at the S&P 500 performance over the last six months and you will see plenty of peaks and valleys.

I read an article recently that blamed the volatility on weak corporate earnings. I had to investigate. I have to admit I did not know the relative strength of corporate earnings right now but that explanation just did not ring true to me. It turns out, nothing could be farther from the truth. Corporate earnings are literally the strongest they have ever been! EVER!

So what in the world is going on? Why is the market so volatile?

Download the full post below - and let me know what you think!

Nightmare on Wall Street 2 - The Fed to the Rescue

I was sitting at my desk in August 2007 reading financial headlines that sounded surreal. I was running a new start-up bank here in Georgia. The Fed was pumping hundreds of billions of dollars into the market in a desperate bid to stabilize them by flushing them full of liquidity – the beginning of a decade-long period of “Quantitative Easing”. The Fed had to do something to keep financial institutions and financial markets from collapsing. I heard that overnight LIBOR rates were not quoted one Friday afternoon. European banks were concerned that if they loaned their excess cash to other banks on Friday, they might not get it back on Monday if the other banks failed. The European Central Bank began pumping hundreds of billions of dollars and Euros into the market. We stood on the cliff-edge of global financial collapse.

In 2007 I had to make sense of what was happening. Why were financial markets spiraling out of control? What did this mean for our little bank? We made loans in our community, mostly to builders. How would these macro events affect us and our borrowers? What did we need to do to prepare for what lay ahead? In fact, the question was what could we do? The answer, it turned out, was nothing. Greenspan had built a monster and no one could control it.

Today, September 18, 2019, I sit at my desk reading the same headlines. Here’s a sample:

The Fed just pumped $128 billion into markets to pull down interest rates

– Business Insider 9/18/19

For a second day, the New York Fed spent billions to calm the financial market

– CNN.com 9/18/19

FED pledges to continue pumping billions into US economy

– BBC.com 9/18/19

Today’s 2019 Fed Monster is of different composition than the Fed Monster birthed in 2007 but no less predictable. How can we say this? Because we blogged about it in 2016: Blog Post October 5, 2016 World Debt Exceeds $152 trillion - Does it even matter to you? and Blog Post October 20, 2016: Here Be Dragons! In hindsight, the 2007 Fed Monster was hiding in plain sight, just as this one has been.

In retrospect, total the Fed pumped $3.5 trillion dollars into financial markets to stabilize them from 2008 to 2015 and despite its best efforts to pare back its balance sheet, it has largely been unsuccessful in its efforts to slime down. And now, in the latest episode of The Fed to the Rescue, market participants know the Fed and ECB will rescue them every time they get into trouble. The decade since the Great Recession has shown that regulators are utterly incapable of de-levering and de-risking financial markets because they themselves are the worst offenders – enormous bloated balance sheets loaded with illiquid assets, drawing money from the treasury at will, disconnected from the restraints that every business on the planet must operate within.

Time will tell if this is going to be another huge “correction.” With age comes wisdom or at least the ability to spot trends. From my chair, the headlines read the same.

Vertical Capital Advisors can help your business plan and execute strategies that enable your enterprise to thrive in all market conditions. It’s not too late to plan. Call us today.